Applying for a mortgage is not a walk in the park, especially when your credit score falls below 740, which is what lenders consider to be a “very good” score. Typically, the higher your score, the lower your interest rates will be. However, if your credit score is on the lower side, don’t lose hope. There are measures you can take to improve it before you apply for a mortgage loan.

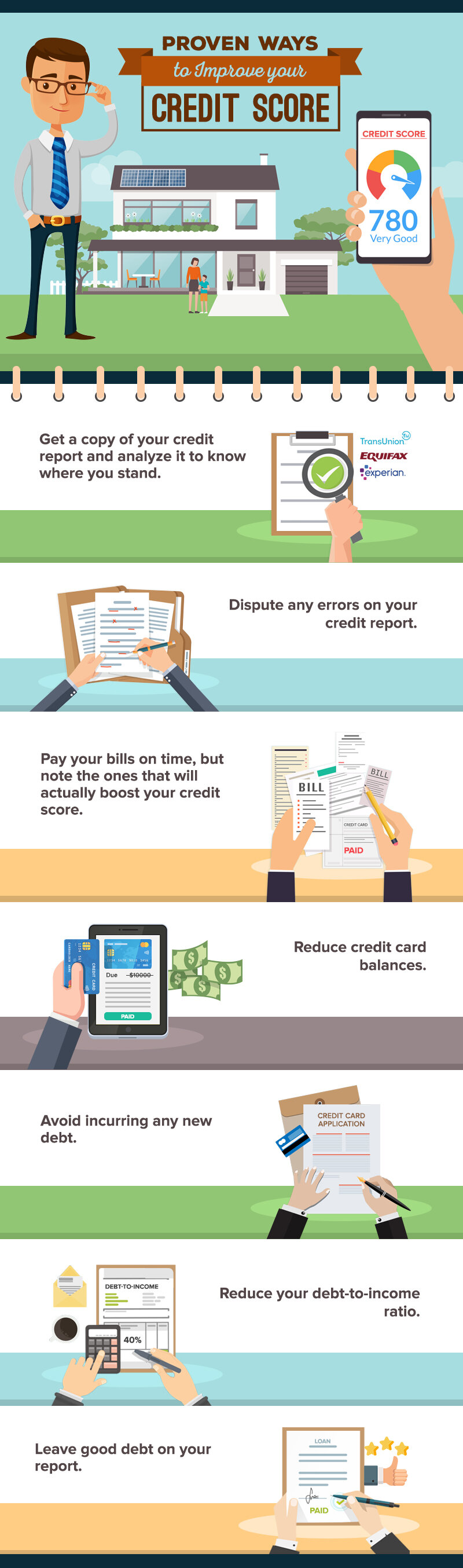

Get a copy of your credit report and analyze it to know where you stand.

When applying for a mortgage loan, the first thing you should do as a homebuyer is to know where you stand in terms of credit. To have a clear idea of your status, you must request a copy of your credit report from the three major reporting agencies (TransUnion, Experian, Equifax).

Having copies of all three reports will allow you to perform an in-depth comparison, as some creditors only send reports to one or two agencies. Getting all three will also make it possible for you to compute your average score – which is likely what a mortgage lender would do to decide if you are qualified for a loan or not.

Ideally, what the mortgage lender should find in your credit report is a solid credit history. Add that to the condition that you should have a steady income and down payment to show – and the pressure can pile up, making the rest of the process of applying for a mortgage even more daunting as it is. However, you’re not alone, and your case isn’t hopeless.

Now that you have analyzed your credit report, you can now work on improving the problem areas to qualify for the best possible mortgage.

Dispute any errors on your credit report.

When you get a hold of your credit report, it is not unlikely for it to contain errors. You may find some inaccurate or incomplete items, as well as some that are out of date, or unverifiable. These kinds of misinformation can be detrimental to your application, so the sooner you can dispute them, the better. Gather supporting documents that can prove your cases and request to have the mistakes either removed or corrected in your report. Also make sure that you follow the correct process.

Pay your bills on time, but note the ones that will actually boost your credit score.

It goes without saying that paying your bills on time is always the best thing to do, and it does help you land more points on your credit score. However, not all bills will have the same positive impact.

According to credit.com, there are on-time payments that won’t directly build up your score no matter how diligent you are in settling them. These bills include rent, utilities, cable, internet, and cell phone bills. Turns out, paying these bills on time won’t land you a higher score – but missing payment on these may hurt your standing. For example, unpaid cable or internet bills that are sent to collections will be put down on record, so it will serve you best to still make on-time payments for any bill.

The ones that directly affect your credit score are credit card bills, student loan payments, mortgage payments, and car payments – so be sure to that you’re able to make timely payments for these if you’re looking to improve your credit score.

Reduce credit card balances.

If you have small balances on several credit cards, you might want to pay these off. Having your credit report polluted with a lot of balances will bring down your credit score and potentially turn off lenders.

Your credit score is affected by how many of your cards have balances, so it’s best to eliminate nuisance balances from separate cards and just choose one or two go-to credit cards that you can use every time you have to make purchases.

Avoid incurring any new debt.

For the lender to see that you are financially stable, do not take on new debt until you’ve been approved for a mortgage. Credit inquiries greatly affect your credit score, so avoid applying for a credit card and making credit-based transactions the same time you’re applying for a mortgage loan.

Reduce your debt-to-income ratio.

Your debt-to-income ratio indicates the percentage of your income that goes into paying your monthly debt. A low debt-to-income ratio means that majority of your income isn’t spent on paying off your debts, whereas a high debt-to-income ratio means that a huge percentage of your income is spent on debt.

If you have a relatively high income, a lender may not view you as much of a risk. However, if your fixed expenses – such as rent and car payments – are also exceptionally high, your income may not help you get a better rate on your mortgage.

To qualify for a good mortgage loan, make sure that your total debt-to-income ratio is 40% or lower. Otherwise, your mortgage underwriter may have some doubts about your ability to make mortgage payments.

Leave good debt on your report.

You may think that leaving a record of debt on your credit report might hurt your chances of getting a good mortgage. When your report shows that you’ve handled your debt well by paying as agreed – that’s a good thing. The more history of good debt you have, the more it helps improve your score.

So, if you’ve had a car loan that’s been paid off or other debt that was correctly settled without the need to involve collection agencies, don’t be in a rush to have these records removed.